The British tax system has always been a source of both confusion and anxiety, particularly for those who have moved into the fixed-income phase of retirement. Recently, headlines regarding a “£420 bank deduction” for UK pensioners have begun circulating, causing a wave of concern across the country. In a world where every penny counts, the idea of an automatic, unexplained grab from your bank account by HM Revenue and Customs (HMRC) is enough to ruin anyone’s morning.

However, as with most things involving the taxman, the reality is far more nuanced than a simple “new rule” or a random deduction. To protect your finances, it is essential to look past the sensationalism and understand why HMRC might be looking at your accounts, how much they are actually entitled to take, and what you can do to keep your money where it belongs.

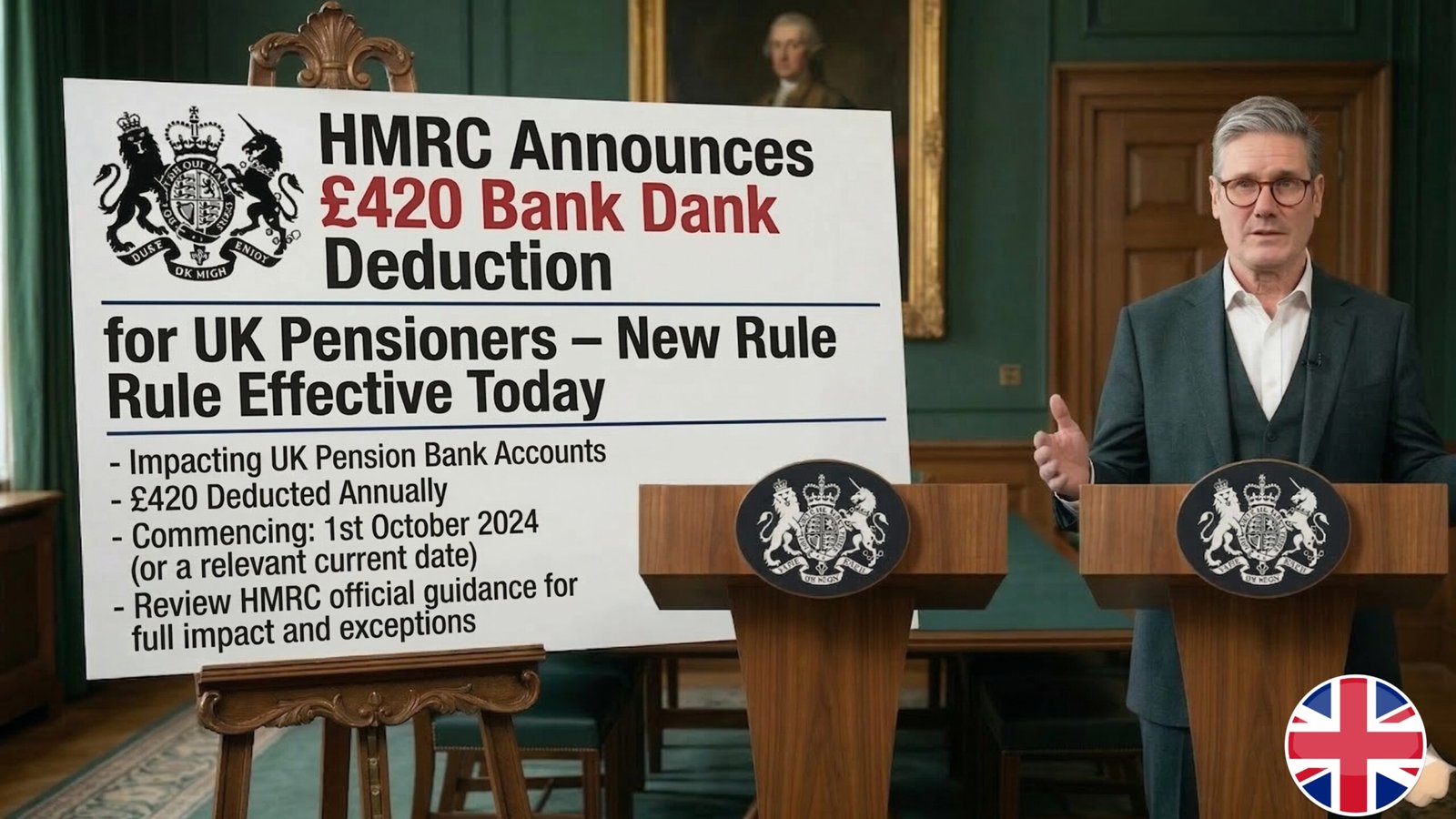

The Truth Behind the £420 Headline

First and foremost, it is important to clarify that HMRC does not have a “new rule” that allows them to arbitrarily pull £420 out of a pensioner’s bank account without warning today. HMRC’s powers to “direct-debit” a person’s bank account (known as Direct Recovery of Debts) are strictly regulated and usually reserved for significant, long-standing tax debts that have been ignored for months.

Good News: £500 Cost of Living Payment Confirmed for March 2026

The figure of £420 is often used in financial examples because it closely mirrors the tax liability for someone who has a small amount of untaxed income—such as savings interest or a small private pension—that exceeds their tax-free allowance. If you have seen this figure mentioned, it is likely referring to a “Simple Assessment” or a “P800” tax calculation where HMRC has determined that, over the course of the last year, you have underpaid your tax by roughly this amount.

Why Pensioners are Suddenly in the Spotlight

For decades, the majority of UK pensioners didn’t have to worry about HMRC. Their state pension and modest savings were well within the tax-free Personal Allowance. However, the financial climate in 2026 has changed the game.

The primary reason more retirees are receiving tax demands is the freezing of the Personal Allowance at £12,570. While the State Pension has increased due to the Triple Lock, the tax-free threshold has remained stagnant. This has created a “fiscal drag” effect, where thousands of pensioners who were previously “tax-free” are now being dragged into the 20% tax bracket. When you add a small private pension or interest from a £10,000 savings account to the mix, a tax bill of £400 to £500 becomes a very real possibility.

How HMRC “Deducts” Money from You

It is a common misconception that HMRC will just “log in” to your bank and take what they want. In reality, HMRC collects underpaid tax from pensioners in three main ways, none of which involve a sudden, unauthorized bank raid.

The most common method is through your Tax Code. If HMRC finds you owe £420, they won’t ask for it in a lump sum. Instead, they will adjust your tax code for the following year. This means that a small amount (roughly £35 per month) will be deducted from your private pension or workplace pension before it even reaches your bank account. This is a “painless” way to pay back the debt, but it does mean your monthly take-home pay will be lower than expected.

Simple Assessment Letters and P800 Forms

If you do not have a private pension that HMRC can adjust via a tax code, they will send you a Simple Assessment (PA302). This is a letter that says, “We have looked at your income, and we think you owe us money.”

This is where the “£420” figure often appears. These letters are sent to people whose income cannot be taxed at the source. If you receive one of these, you are given a deadline (usually January 31st of the following year) to pay the balance. While it feels like a “deduction,” you are actually the one in control of making the payment. Ignoring these letters is the only way you would ever reach the stage where HMRC takes legal action to recover the funds directly from your assets.

The Role of Savings Interest in Tax Bills

Many UK pensioners have spent their lives saving for a rainy day. With interest rates in 2026 being more favorable than they were five years ago, those savings are finally generating income. However, the Personal Savings Allowance (PSA) is only £1,000 for basic-rate taxpayers.

If you have £15,000 in a savings account paying 4% interest, you are earning £600 a year. If your total income is already above the Personal Allowance, that £600 is “untaxed income.” Banks report this interest directly to HMRC. If you have multiple accounts, those small amounts add up. Suddenly, HMRC realizes you’ve earned more than your allowance, and they send a notice for the tax owed—which, coincidentally, can often sit right around that £400 to £500 mark.

Identifying Potential Errors in Your Tax Bill

Before you reach for your checkbook or accept a tax code change, you must verify that HMRC’s numbers are correct. HMRC’s automated systems are efficient, but they are not infallible. They often make assumptions based on “estimated” income that may not reflect your current reality.

Common errors include:

-

Double Counting: Sometimes a pension provider and HMRC both report the same income separately.

-

ISA Interest: Interest earned in a Cash ISA or Stocks & Shares ISA is tax-free, but sometimes banks accidentally report it as taxable.

-

Joint Accounts: If you have a joint account with a spouse, the interest should be split. HMRC sometimes attributes 100% of the interest to one person, doubling their tax liability.

What to Do if You Receive a Notice Today

If a letter from HMRC arrived today, your first step should be to stay calm. You are not under investigation; you are simply part of a massive administrative cleanup that happens every year as HMRC reconciles the previous year’s data.

Gather your P60 (the annual statement from your pension provider) and your bank interest certificates. Compare these to the figures in the HMRC letter. If there is a discrepancy, you can use the HMRC Personal Tax Account online to challenge the figures. This digital portal is the fastest way to correct errors and often results in the “deduction” being cancelled or significantly reduced.

Avoiding Future “Surprise” Tax Bills

The best way to stop HMRC from sending you demands for £420 is to be proactive about your tax-efficiency. For many pensioners, the simplest solution is to move taxable savings into an ISA. By doing this, you legally remove that interest from HMRC’s view, effectively lowering your taxable income.

Another strategy is to monitor your “Triple Lock” increases. Every time the State Pension goes up, you move closer to the tax threshold. If you know you are going to be £50 over the limit, you can contact HMRC and ask them to adjust your tax code early. This prevents a “catch-up” bill at the end of the year, which is usually when these large, scary figures appear.

The Myth of the “Automatic Bank Deduction”

To be absolutely clear: there is no “New Rule” effective today that allows HMRC to bypass the legal process and take £420 from your bank. If you see a notification on social media or in a dubious email claiming that a deduction has been made, do not click any links.

Scammers frequently use HMRC’s name and specific figures like “£420” to trick people into giving up their banking details. They know that pensioners are worried about tax changes and use that fear to gain access to accounts. Real HMRC communications will almost always come via the post (the famous brown envelope) or through your official “Government Gateway” account.

How to Contact HMRC for Support

If you are struggling to understand a tax notice, there are resources available specifically for retirees. Organizations like TaxHelp for Older People provide free, independent advice for those on lower incomes. They can help you talk to HMRC and ensure you are claiming all the allowances you are entitled to, such as the Marriage Allowance or the Blind Person’s Allowance, which can often wipe out a tax bill entirely.

HMRC also has a dedicated helpline for pensioners. While wait times can be long, speaking to a human being can often resolve a “Simple Assessment” issue in minutes. They can explain exactly which piece of data triggered the bill and, if you genuinely owe the money, they can set up a manageable payment plan.

Summary of Your Rights and Responsibilities

As a UK pensioner in 2026, you have the right to a clear explanation of any tax you owe. You are not required to pay any “deduction” that you haven’t been given a chance to contest. While the “£420” figure might be a common outcome of the current tax freezes, it is not an inevitable penalty.

By staying organized and understanding the intersection of your pension and your savings interest, you can navigate these HMRC notices with confidence. Remember, the goal of the tax system is to collect what is owed, not to leave you in financial hardship. If a bill seems wrong, it probably is—and you have every right to fight it.