The UK pension landscape is currently buzzing with speculation, hope, and a fair share of skepticism. For millions of retirees across the country, the State Pension isn’t just a government benefit; it is the bedrock of their financial security. Recently, headlines have been circulating suggesting a massive shift that could see over-60s receiving as much as £2,344 per month. But how much of this is grounded in immediate policy, and what does it actually mean for the average person navigating the cost-of-living crisis?

Understanding the complexities of the Department for Work and Pensions (DWP) regulations is a full-time job in itself. With the Triple Lock mechanism constantly under the microscope and the transition from the Basic State Pension to the New State Pension still causing confusion, it’s vital to break down what is actually happening. This review of pension rates isn’t just about numbers on a spreadsheet; it’s about the dignity of aging in a volatile economy.

The Reality of the Triple Lock System

To understand any potential increase, we first have to look at the Triple Lock. Introduced to ensure that pensioners don’t see their purchasing power eroded by inflation, the Triple Lock guarantees that the State Pension rises every April by whichever is the highest of three figures: average earnings growth, inflation (measured by the Consumer Price Index), or a flat 2.5%.

In recent years, this has led to some of the most significant jumps in pension history. However, the figure of £2,344 per month represents a substantial leap from current levels. For this to become a reality, we would need to see a combination of high wage growth and a government commitment to significantly “uplift” the base rate beyond the standard Triple Lock calculations. While the government remains committed to the Triple Lock for now, the debate in Westminster often shifts toward whether this model is sustainable in the long term.

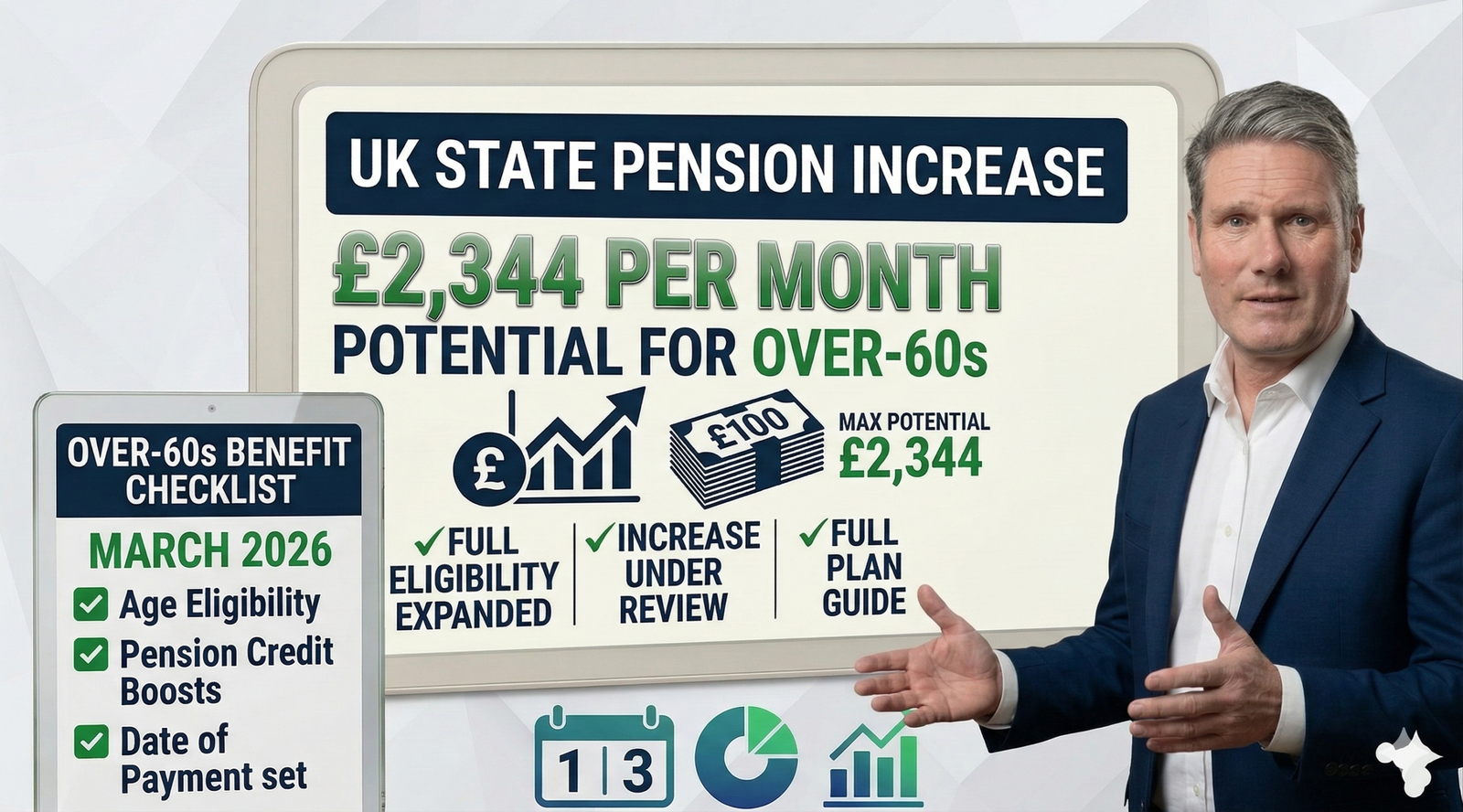

Breaking Down the £2,344 Figure

When people see a figure like £2,344 per month, the first question is usually: “Is that for everyone?” Currently, the full New State Pension sits significantly lower than that. For a monthly payment to reach over £2,300, we would be looking at a total annual pension of roughly £28,128.

UK Ends the 67 Rule – New State Pension Age Officially Approved

To put that in perspective, the current full New State Pension is roughly £11,502 per year. Moving to £28,000 would essentially more than double the current payout. While there are various campaigns—such as those by Silver Voices and other advocacy groups—calling for the State Pension to be aligned with the National Living Wage, a jump of this magnitude would require a complete overhaul of the UK’s fiscal policy. It is more likely that such figures represent a “target” or a “best-case scenario” discussed in radical policy reviews rather than an imminent change scheduled for the next fiscal year.

The Impact of the Cost of Living

The reason these rumors of a massive increase gain so much traction is simple: the current rates are a struggle for many. Even with the recent 8.5% increase, many UK pensioners find themselves choosing between heating and eating. Energy bills remain high, and food inflation, while cooling, has already set a new, higher baseline for weekly grocery shops.

For an individual over 60, a monthly income of £2,344 would be life-changing. It would move the State Pension from a “survivalist” payment to a “comfortable” one. Currently, the UK has one of the least generous state pensions when compared to average earnings among OECD nations. This gap is what fuels the fire for a major review. The public sentiment is clear: if the UK is to be a world-leading economy, its treatment of its eldest citizens must reflect that wealth.

Eligibility and the Age Threshold

One of the most contentious points in the current pension review is the age of eligibility. We have seen a steady climb in the State Pension age, moving from 65 to 66, and eventually heading toward 67 and 68. The mention of “over-60s” in these new proposals is particularly interesting because it suggests a potential lowering of the age threshold or a specific “early access” window for those in demanding physical jobs.

However, current UK law doesn’t allow you to claim the State Pension at 60. Most people at that age are relying on private pensions or workplace schemes to bridge the gap until they hit 66 or 67. If a review truly considers providing a substantial monthly sum to those over 60, it would mark one of the most significant reversals in social policy in decades. It would acknowledge that for many, working into their late 60s simply isn’t a physical or practical reality.

New State Pension vs Basic State Pension

We cannot talk about an increase without addressing the “two-tier” system. Those who reached pension age before April 6, 2016, are on the old Basic State Pension, while those after are on the New State Pension. The New State Pension is generally higher, but it requires 35 qualifying years of National Insurance contributions to get the full amount.

Any review aiming for a £2,344 monthly payment would have to address the disparity between these two groups. Would the increase apply to everyone, or just those on the new system? Historically, those on the older system feel left behind, as their inflationary increases are calculated on a lower base rate. A fair review would need to consolidate these systems to ensure that an 80-year-old isn’t receiving significantly less than a 67-year-old for the same lifetime of work.

The Role of National Insurance Contributions

To get anywhere near the maximum state pension, your National Insurance (NI) record must be spotless. Many people reach retirement age only to find they have “gaps” in their record due to years spent raising children, caring for relatives, or working abroad.

If the government were to move toward a higher monthly payment, the rules around NI years might become even stricter. Alternatively, there is a push to allow people to “buy back” more years or to credit those who performed unpaid labor (like caregiving) more heavily. For the average UK citizen, checking your NI record on the government gateway is the first step in seeing if you’d even qualify for the top-tier rates being discussed in these reviews.

Inflation and the Economic Backdrop

The UK economy has been on a rollercoaster. With the Bank of England fluctuating interest rates to curb inflation, the “real-world” value of a pension is constantly changing. A 10% increase sounds great on paper, but if the price of bread and milk has gone up by 12%, the pensioner is effectively poorer.

The review currently under discussion looks at how to “future-proof” payments. If a figure like £2,344 is being floated, it is likely based on a projection of what a “living pension” should look like in a post-inflationary world. Economists argue that a static pension is a dying pension. For the over-60s to have true financial peace of mind, the payments must be indexed in a way that accounts for the specific spending patterns of the elderly, which often lean more heavily on heating and healthcare than the general population.

Private Pensions and the Gap

While the State Pension is the focus, we must acknowledge that it was never designed to be the sole source of income for most people. The UK’s “Automatic Enrolment” scheme has helped millions save into private workplace pensions, but there is a “forgotten generation”—those now in their 60s and 70s—who didn’t benefit from these schemes for the majority of their careers.

For these individuals, the State Pension is everything. A review that pushes the payment toward a more livable monthly sum would reduce the reliance on Pension Credit and other means-tested benefits. It’s a matter of administrative efficiency as much as it is of social justice. By paying a higher flat rate, the government could potentially save billions in the administration of complex top-up benefits.

The Political Will for Change

Any mention of a “pension review” eventually lands at the door of 10 Downing Street. With a general election always on the horizon in the British political cycle, pensions are a powerful tool. Older voters are the most consistent demographic at the polls, making their financial well-being a top priority for any party looking to hold power.

However, the Treasury is often at odds with the DWP. The Treasury looks at the aging population and sees a growing “liability,” while the DWP looks at the same population and sees a growing need. For a monthly payment of £2,344 to be approved, there would need to be a seismic shift in how the UK views its social contract. It would require viewing the pension not as a “cost” to be managed, but as an “investment” in the silver economy.

Challenges to the Proposed Increase

It would be remiss not to mention the obstacles. The primary hurdle is, of course, the “black hole” in public finances. Critics of large pension increases often point to “intergenerational unfairness,” arguing that younger workers, who are struggling with astronomical housing costs and student debt, shouldn’t be taxed further to fund a higher standard of living for the retired.

This tension is the main reason why such high figures are often “under review” but rarely implemented overnight. The government must balance the books. To fund a £2,000+ monthly pension, NI contributions for current workers would likely have to rise, or other services—like the NHS or education—would face cuts. This is the delicate balancing act that keeps the State Pension at its current, more modest level.

What Should You Do Now?

While the talk of £2,344 per month is exciting, it is important to stay grounded in current realities while preparing for the future. The best thing any UK resident over 60 (or approaching that age) can do is to conduct a thorough financial audit.

First, get a State Pension forecast from the GOV.UK website. This will tell you exactly how much you are on track to receive based on your current NI contributions. Second, check if you are eligible for Pension Credit. Thousands of people miss out on this “gateway benefit” which not only tops up your income but also unlocks help with heating bills and Council Tax. Even if the state doesn’t suddenly double your pension, ensuring you are getting every penny you are currently entitled to is vital.

Looking Toward the Future

The conversation around the UK State Pension is changing. We are moving away from asking “how little can we give?” to “how much is needed for a dignified life?” The review of pension rates is a sign that the government acknowledges the current system is under strain.

Whether the figure eventually lands at £2,344 or a more conservative increase, the trajectory is clear: the status quo is no longer enough. As the UK continues to navigate its post-Brexit, post-pandemic identity, how it cares for its retirees will be the ultimate litmus test of its values. For now, keep an eye on the Spring and Autumn statements, as these are the moments when “reviews” turn into “reality.”