The Department for Work and Pensions has officially moved forward with one of the most significant adjustments to disability benefits in recent years. As we enter March 2026, millions of claimants across the United Kingdom are beginning to see the practical effects of the annual uprating on their bank balances. With the cost of living still a major talking point in households from Glasgow to London, these new figures offer a much-needed breakdown of what people can actually expect to receive. This isn’t just a minor tweak to the system; for those on the highest tiers of support, the monthly total is now reaching levels that provide a much stronger safety net than in previous cycles.

Understanding the headline figure

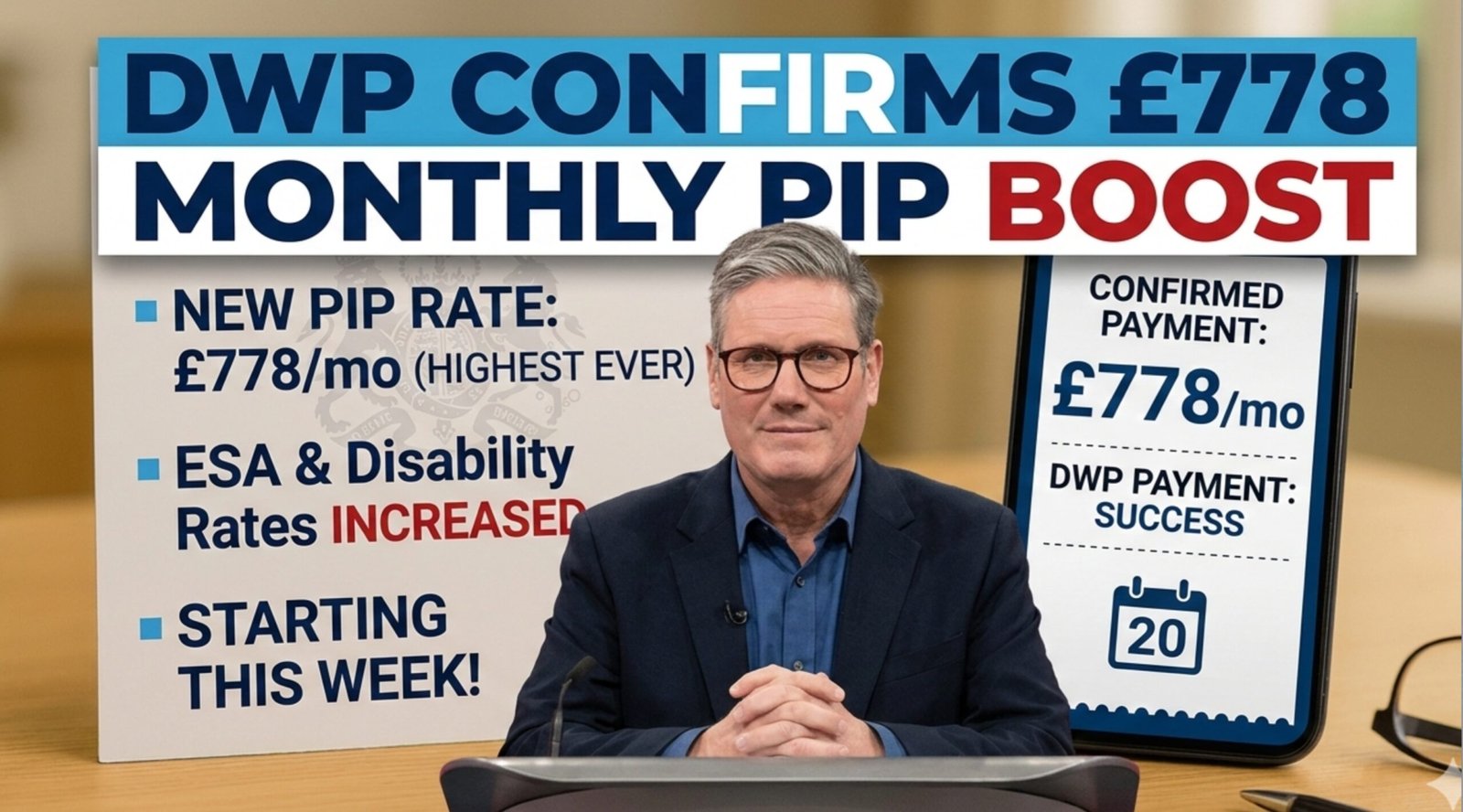

When people hear about a seven hundred and seventy-eight pound monthly payment, it often sounds like a single flat rate. In reality, this figure represents the maximum combined award for Personal Independence Payment, often referred to as PIP. Specifically, it applies to those who have been assessed as needing the enhanced rate for both the daily living and the mobility components.

For the 2026/2027 financial year, the weekly rate for the enhanced daily living component has risen to one hundred and fourteen pounds and sixty pence. When you add the eighty pounds per week for the enhanced mobility component, the weekly total hits one hundred and ninety-four pounds and sixty pence. Since PIP is typically paid every four weeks, this brings the total periodic payment to seven hundred and seventy-eight pounds and forty pence. This increase is a direct response to the inflationary pressures recorded in late 2025, ensuring that the purchasing power of the most vulnerable is not completely eroded by the rising cost of services and specialized equipment.

The rollout schedule for March 2026

One of the most frequent questions arriving at the DWP helplines this week is regarding the exact date these new amounts will appear. While the official “uprating” date for the new financial year is usually in April, the administrative groundwork and the first set of adjusted payments often begin to overlap with the final weeks of March.

Because PIP and other disability benefits are paid in cycles—usually every four weeks on a specific weekday—not everyone will see the change on the exact same morning. If your payment was due on a Monday, you might see the adjustment slightly earlier than someone whose cycle ends on a Friday. The DWP has confirmed that their systems are now processing these updated rates, meaning that for many, the very next payment landing in their account will reflect these higher amounts. It is worth noting that if your payment period straddles the old and new rate dates, you might receive a “pro-rata” payment, which is a mix of both rates, before the full increase kicks in during the following month.

Breakdown of the new PIP daily living rates

PIP is divided into two parts, and the daily living component is designed to help with the extra costs of managing a long-term health condition or disability in the home. This could include help with preparing food, managing medication, or communicating with others.

Under the new 2026 rates, the standard rate for daily living has moved up to seventy-six pounds and seventy pence per week. This is an increase from the previous year’s seventy-three pounds and ninety pence. For those on the enhanced rate, as mentioned, the new figure is one hundred and fourteen pounds and sixty pence. These increases might seem small on a weekly basis, but over the course of a year, they add hundreds of pounds to a claimant’s budget, which can be the difference between struggling and managing effectively.

New mobility component figures for 2026

The second part of PIP is the mobility component, which looks at how much help you need getting around. This is often the part of the benefit that allows people to access the Motability Scheme or pay for specialized transport.

For the standard mobility rate, the weekly amount has increased to thirty pounds and thirty pence. For those who require the enhanced mobility rate, the payment is now eighty pounds per week. Many claimants find that the mobility portion is the most critical part of their award, as it directly impacts their ability to maintain independence, attend medical appointments, and participate in community life. The jump to eighty pounds represents a clear acknowledgement from the DWP that transport costs—from fuel to public transit fares—have seen sharp increases over the last twelve months.

ESA and the work-related activity group

While PIP is often the most talked-about benefit because it is not means-tested, Employment and Support Allowance remains a lifeline for those whose disability or health condition limits their ability to work. For those in the Work-Related Activity Group, the rates have seen a steady climb.

The personal allowance for a single claimant aged twenty-five or over has increased to ninety-five pounds and fifty-five pence per week. On top of this, the component for the Work-Related Activity Group has risen to thirty-seven pounds and ninety-five pence. This brings the weekly total for many in this category to over one hundred and thirty-three pounds. The goal of this support is to provide financial stability while the individual engages in activities that might eventually help them move back toward the workforce, though the DWP recognizes that for many, this is a long-term or even permanent situation.

Support group increases for ESA claimants

For those ESA claimants who are placed in the Support Group—meaning the DWP has determined they cannot realistically be expected to work or look after their health at the same time—the rates are even higher.

The Support Group component has increased to fifty pounds and thirty-five pence per week. When combined with the standard personal allowance, these claimants are looking at a weekly income of one hundred and forty-five pounds and ninety pence from ESA alone. It is important to remember that many people in the Support Group are also eligible for the highest rates of PIP. When you combine these two benefit streams, the total monthly support can be substantial, reflecting the high cost of living with severe, long-term health challenges in the current UK economy.

Disability Living Allowance and Attendance Allowance

Although PIP is the main benefit for working-age adults, many people are still on Disability Living Allowance or receive Attendance Allowance if they are over the State Pension age. The DWP has confirmed that these rates are also rising in tandem.

Attendance Allowance, which helps with extra costs if you have a disability severe enough that you need someone to look after you, now has a higher rate of one hundred and fourteen pounds and sixty pence and a lower rate of seventy-six pounds and seventy pence per week. These match the PIP daily living rates, ensuring that the level of support remains consistent regardless of whether the disability was identified before or after retirement age. This alignment is crucial for fairness within the system, ensuring that seniors aren’t left behind as benefit rates are updated.

The impact of the September 2025 CPI

The reason these rates have landed at these specific figures is tied back to the Consumer Price Index from September 2025. By law, the DWP must review the value of disability benefits every year to ensure they don’t lose their value against inflation.

The inflation figure recorded last autumn was approximately three point eight percent. While some politicians and advocacy groups argued for a higher “social” inflation rate—noting that disabled people often spend a higher proportion of their income on energy and specialized food—the government stuck to the standard CPI link. This three point eight percent increase has been applied across the board to PIP, ESA, DLA, and Carer’s Allowance. While it may not cover every single price hike an individual faces, it represents a multi-billion pound commitment from the Treasury to maintain the disability support framework.

Why some people might see different amounts

It is a common source of confusion when two people on the “same” benefit receive different amounts. This usually comes down to the complex web of premiums and “passported” benefits. For example, if you are on ESA and also receive the Severe Disability Premium, your weekly amount will be significantly higher than someone without that premium.

For 2026, the Severe Disability Premium has risen to eighty-six pounds and five pence per week for a single person. These “premiums” are essentially top-ups for people who live alone and don’t have a carer claiming Carer’s Allowance for them. They are designed to acknowledge that living alone with a disability is inherently more expensive than living in a household where care can be shared. If your payment doesn’t seem to match the standard rates, it is always worth checking if you have been awarded—or should be awarded—one of these additional premiums.

Moving from old benefits to Universal Credit

We are also in the middle of a massive administrative shift known as “Managed Migration.” This is the process where the DWP moves people from “legacy” benefits like Income-related ESA over to Universal Credit.

If you have received a migration notice this week, it is vital not to ignore it. The DWP has built in “transitional protection” to ensure that people don’t lose money at the point of transfer. This means if your old ESA rate was higher than the new Universal Credit rate, the DWP will add a top-up to your Universal Credit to make up the difference. However, this protection only applies if you follow the migration instructions and apply by the deadline. For many disability claimants, this transition is the biggest change to their financial life in a decade, and the new 2026 rates are being baked into this new Universal Credit structure from the start.

The role of Carer’s Allowance in 2026

We cannot talk about disability rates without mentioning the people who provide the care. Carer’s Allowance has also seen an increase, now standing at eighty-six pounds and forty-five pence per week.

Crucially, the earnings threshold—the amount a carer can earn from a part-time job without losing their allowance—has also been adjusted. For the 2026/2027 year, this threshold has been raised to two hundred and four pounds per week. This is a significant move, as it allows carers to take on a few more hours of work or benefit from a pay rise in their job without being hit by the “cliff edge” where their entire Carer’s Allowance is withdrawn. This change has been long-campaigned for by disability charities and represents a win for household budgets that rely on a mix of benefits and earned income.

How to verify your new payment amount

If you want to be certain about what you are going to receive, the best place to look is your most recent “Annual Uprating” letter from the DWP. These letters are usually sent out between February and March every year.

The letter will break down exactly which components you are receiving and what the new weekly rate will be. If you haven’t received your letter yet, don’t worry—the post can be slow during these high-volume periods. You can also check your online portal if you are on Universal Credit, as the “Payment Statement” section will be updated with the new figures as soon as your next assessment period ends. Keeping these letters in a safe place is important, especially if you need to provide proof of income for a mortgage, a rental agreement, or a council tax discount application.

Staying safe from benefit-related scams

As with any major news regarding DWP payments, scammers are currently very active. They often send out texts or emails that look official, claiming that you need to “sign up” or “verify your identity” to receive the new seven hundred and seventy-eight pound rate.

The most important thing to remember is that the DWP will never ask for your bank details or personal information via a text message link. These rate increases are applied automatically. You do not need to “claim” the increase; if you are already on the benefit, the system will update itself. If you get a suspicious message, the best thing to do is delete it and check your official DWP online account or call the official PIP enquiry line. Never give out your National Insurance number or bank login details to someone who has contacted you out of the blue.

Looking toward the future of disability support

As we look at the remainder of 2026, the conversation around disability benefits is unlikely to quiet down. There are ongoing discussions about how the DWP carries out assessments and whether the current system of “descriptors” accurately captures the challenges of mental health conditions versus physical ones.

However, for today, the focus for most claimants is on the immediate financial relief provided by these new rates. The transition to the 2026 figures marks a period of stability after a few very volatile years. While no system is perfect, the confirmation of these increases—and the fact that they are starting to hit bank accounts this week—provides a clear framework for disabled people and their families to plan their finances for the year ahead.