The British retirement landscape is currently undergoing a quiet but significant transformation. For decades, the State Pension was generally seen as a tax-free benefit for most, as the amount received sat comfortably below the threshold of the Personal Allowance. However, as we approach the new tax year in April 2026, HM Revenue and Customs (HMRC) has clarified a reality that many retirees are only just beginning to grasp: more pensioners than ever before are set to become taxpayers.

This shift isn’t due to a sudden new “pension tax” but rather a combination of rising pension payments and a frozen tax-free ceiling. If you are a UK pensioner, or are about to become one, understanding how these rules intersect is no longer optional—it is a financial necessity to avoid unexpected bills and penalties.

The Collision of Triple Lock and Frozen Thresholds

The core of the issue lies in two opposing government policies. On one hand, we have the Triple Lock, a mechanism designed to protect the value of the State Pension by increasing it annually by whichever is highest: inflation, average earnings growth, or 2.5%. For the 2026/27 tax year, this has resulted in a substantial 4.8% boost to payments.

Good News: £500 Cost of Living Payment Confirmed for March 2026

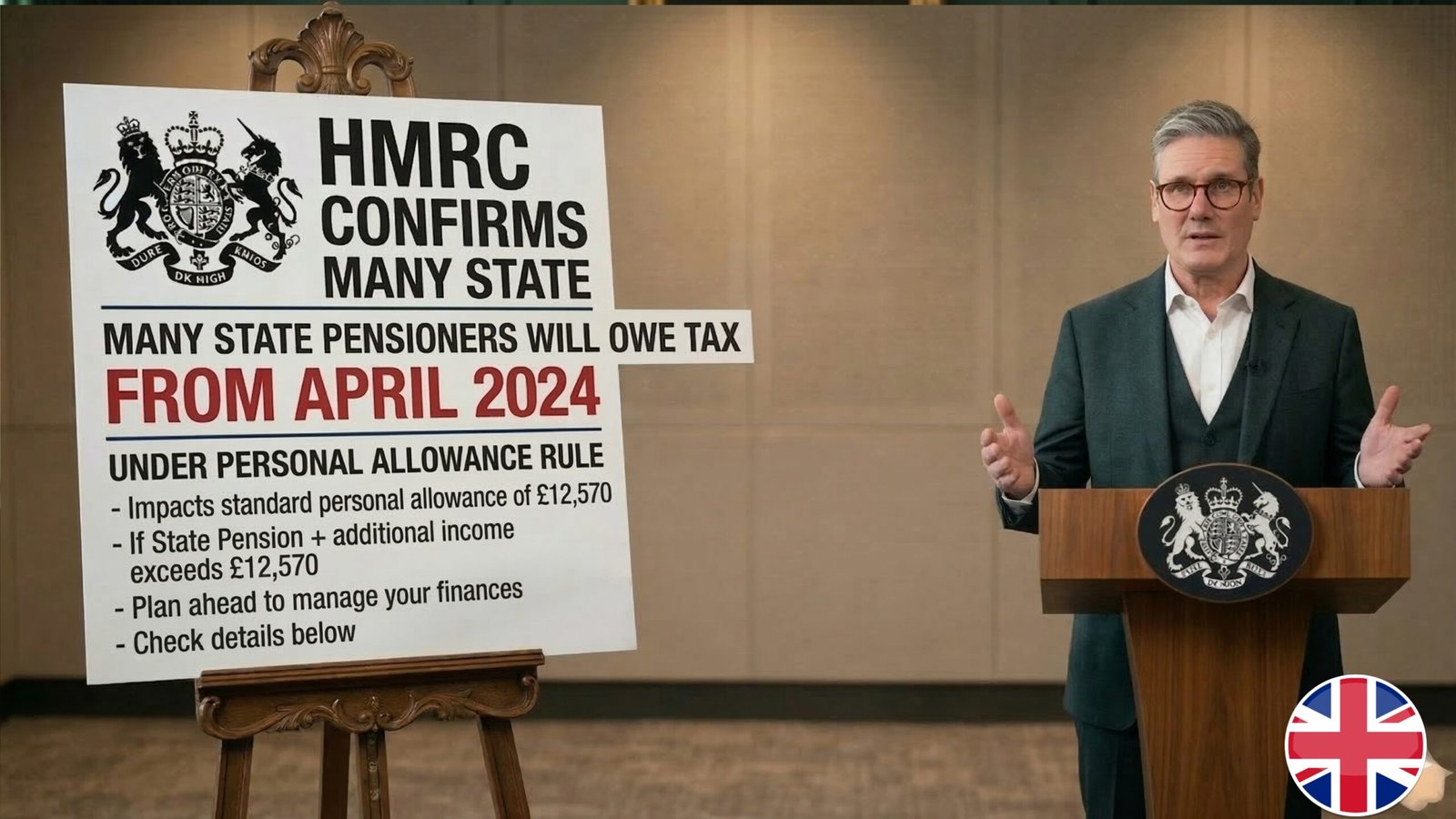

On the other hand, the Personal Allowance—the amount of income you can earn before paying a single penny in tax—has been frozen at £12,570 per year. This freeze has been in place since 2021 and, following recent budget announcements, is now expected to remain at this level until at least 2031. As the State Pension rises to meet the cost of living, it is rapidly “drifting” toward this static tax-free limit. This phenomenon, known as fiscal drag, is effectively pulling hundreds of thousands of retirees into the tax net every year.

Breaking Down the 2026 Pension Figures

To understand why April is a turning point, we have to look at the numbers. The full New State Pension is set to rise to approximately £12,548 per year for the 2026/27 cycle. When you compare this to the Personal Allowance of £12,570, the margin of safety has almost vanished. There is now a gap of just £22.

For a pensioner whose only source of income is the State Pension, they remain technically under the tax threshold. However, very few people rely solely on the state. If you have a small private pension, a part-time job, or even modest interest from a savings account that exceeds £22 over the entire year, you will officially owe income tax. HMRC’s data suggests that by the end of this tax year, the number of pensioners paying income tax will have risen by nearly one million compared to just three years ago.

How HMRC Collects Tax from Pensioners

One of the most common points of confusion is how this tax is actually paid. Most workers are used to the PAYE (Pay As You Earn) system, where tax is deducted before the money hits their bank account. For pensioners, it works slightly differently. HMRC does not usually deduct tax directly from the State Pension itself.

Instead, they use your Tax Code. If you have a private or workplace pension, HMRC will adjust the tax code on that second income. They will “instruct” your private pension provider to take a larger slice of tax to cover what is owed on your State Pension. If you do not have a private pension but have other forms of income, such as rental income or significant savings interest, HMRC may issue a Simple Assessment. This is a letter sent after the end of the tax year telling you exactly how much you owe, which you must then pay manually.

The Impact on the Basic State Pensioners

It is not just those on the “New” State Pension (those who retired after April 2016) who are affected. Those on the Basic State Pension—the older system—are also seeing their margins shrink. While their base rate is lower, many of these retirees receive “Additional State Pension” (such as SERPS).

When these additional payments are added to the annual increase, many “old system” pensioners find their total state income already exceeds the £12,570 limit. For this group, tax has already become a reality, but the April 2026 increase will see their tax bills climb higher as a larger portion of their income falls into the 20% basic rate bracket.

Why Savings Interest is Now a Tax Trigger

For many years, pensioners could keep a healthy amount of cash in a standard savings account without worrying about HMRC. This was because interest rates were near zero. Today, with rates much higher, that same “nest egg” is generating taxable income.

The Personal Savings Allowance allows basic-rate taxpayers to earn £1,000 in interest tax-free. However, to qualify for that £1,000 allowance, you must first be a “taxpayer.” Because the rising State Pension is using up almost all of your £12,570 Personal Allowance, your savings interest no longer has any “tax-free” room left within the main allowance. If your total income (pension + interest) goes over the limit, you may find that HMRC adjusts your tax code specifically to account for the interest earned on your bank accounts.

The Role of the Starting Rate for Savings

There is a small silver lining known as the Starting Rate for Savings. This is a special 0% tax rate that applies to up to £5,000 of savings interest for people with low overall incomes.

The rule is specific: for every £1 your “other income” (like your pension) goes above the Personal Allowance, your £5,000 starting rate is reduced by £1. Because the New State Pension is now so close to the £12,570 limit, most pensioners will still be able to use a large portion of this £5,000 buffer. However, once your total pension income (state plus private) exceeds £17,570, this special safety net disappears entirely. Understanding where you sit on this sliding scale is essential for planning your 2026 finances.

The “Hidden” Costs of Becoming a Taxpayer

Becoming a taxpayer for the first time in retirement isn’t just about the money lost to the Exchequer; it’s about the administrative burden. Many pensioners have not had to deal with HMRC for decades. The arrival of a P800 tax calculation or a Simple Assessment letter can be deeply stressful.

Furthermore, being a taxpayer can affect eligibility for other localized benefits. Some council-based support schemes or grants use “net income” or “tax status” as a benchmark for eligibility. While the State Pension increase is intended to help with inflation, the fact that a portion of it is immediately clawed back via tax means that the “real-world” benefit to the pensioner is less than the headline 4.8% figure suggests.

Simple Steps to Manage Your Tax Position

If you are worried about the April changes, there are proactive steps you can take. The most effective is the use of ISAs (Individual Savings Accounts). Any interest earned inside an ISA is completely invisible to HMRC and does not count toward your tax thresholds. If you have savings in a standard account, moving them into a Cash ISA can simplify your tax affairs significantly.

Another option is to check your National Insurance record. If you are still working part-time or have multiple income streams, ensuring your tax codes are allocated to the correct provider can prevent “emergency tax” from being taken. HMRC’s online “Personal Tax Account” is a surprisingly useful tool for this, allowing you to see exactly how they are calculating your liability before the April deadline arrives.

What to Do if You Receive an HMRC Notice

If a letter from HMRC arrives this April, don’t ignore it. The system is largely automated, and errors do occur. Banks sometimes report interest incorrectly, or HMRC might not be aware that a portion of your income is actually tax-exempt.

If you receive a Simple Assessment (PA302), you have 60 days to challenge it if you believe the figures are wrong. For many older people, the complexity of these forms is overwhelming. Charities like TaxHelp for Older People provide free, independent advice to those on lower incomes. They can help you navigate the jargon and ensure you aren’t paying a penny more than the law requires.

The Long-Term Outlook for UK Retirees

The trend of more pensioners paying tax is unlikely to reverse anytime soon. As long as the Triple Lock remains in place and the Personal Allowance remains frozen, we will see a “squeezing” effect. Within the next few years, it is highly probable that the full New State Pension will actually exceed the Personal Allowance.

When that happens, the government will face a choice: either raise the tax threshold or implement a system to tax the State Pension at source for everyone. Until then, the responsibility falls on the individual to keep their house in order. April 2026 marks the beginning of a new era where “pensioner” and “taxpayer” are no longer separate categories for the majority of the UK population.

Final Thoughts on the April Transition

The confirmation from HMRC is a wake-up call. While the 4.8% increase in the State Pension is a positive step for retirement security, it comes with strings attached. By understanding the £12,570 limit and how your various income streams—from private pensions to savings interest—interact with it, you can take the sting out of the “April Tax Trap.”

Retirement should be a time of peace, not paperwork. A little bit of preparation now can ensure that when the new tax year begins, you are focused on enjoying your increased pension rather than worrying about a surprise letter from the taxman.