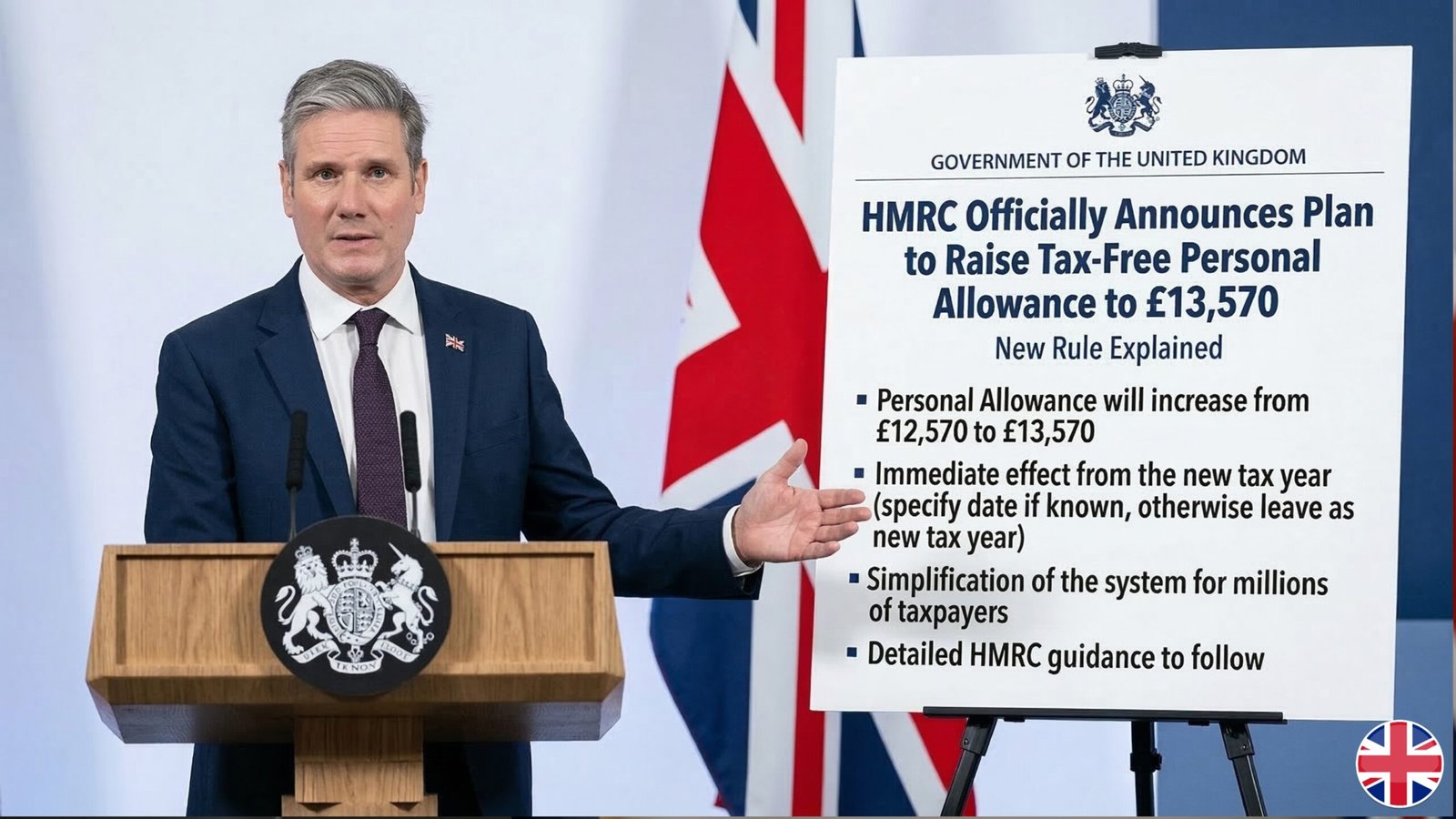

In the world of UK finance, few things spark as much conversation as a change to the Personal Allowance. It is the bedrock of our tax system—the amount of money every individual can earn before the taxman takes a slice. Recently, headlines have been swirling across social media and news outlets claiming that HM Revenue and Customs (HMRC) is officially raising this threshold to £13,570 for the 2026/27 tax year.

For millions of workers and pensioners struggling with the cost of living, such a rise would be a lifeline. However, as we look closer at the official government data and the recent Spring Budget updates, the reality is far more complex. While there is immense pressure on the Chancellor to provide tax relief, the official stance on the “tax-free” limit remains a point of significant contention.

The Reality of the £12,570 Threshold

To understand the current situation, we must look at the facts as they stand today. Since 2021, the Personal Allowance in the UK has been frozen at £12,570. This freeze was originally intended to be a temporary measure to help repair the national balance sheet following the pandemic. However, subsequent budgets have extended this freeze, with the current legislation keeping it locked until at least April 2028.

When you hear rumors of an increase to £13,570, it is often based on what the allowance should be if it had risen in line with inflation (CPI). By keeping the threshold at £12,570 while wages and pensions rise, the government is engaging in what economists call “fiscal drag.” This essentially means that as your pay goes up to keep pace with inflation, a larger portion of your income falls into the taxable bracket, resulting in a “stealth” tax rise.

Why the £13,570 Figure is Circulating

The figure of £13,570 isn’t just a random number plucked from thin air. It represents a hypothetical 8% increase on the current threshold—a figure that many campaign groups and backbench MPs have been lobbing for to offset the impact of the high inflation seen in 2024 and 2025.

If HMRC were to announce such a plan, it would mean an extra £1,000 of tax-free income for every basic-rate taxpayer. For someone earning £30,000 a year, this would result in an annual tax saving of approximately £200. While HMRC carries out the administration of tax, the actual decision to change these “rules” lies solely with the Treasury and the Chancellor of the Exchequer. As of the latest 2026 updates, there is no confirmed legislation to move the needle from £12,570 to £13,570, despite the intense public demand.

Impact on the Triple Lock Pensioners

The group most affected by the current freeze is the UK’s pensioner population. Under the Triple Lock, the State Pension has seen significant increases over the last two years. In April 2026, the New State Pension is set to rise to approximately £12,548 per year.

You will notice that this figure is just £22 shy of the £12,570 Personal Allowance. This means that if the government does not raise the threshold to £13,570 or similar, almost every pensioner receiving the full New State Pension will be on the verge of becoming a taxpayer. Any additional income—be it a small private pension or even modest interest from a savings account—will suddenly trigger an HMRC tax demand. This is why the rumor of a threshold increase is so popular; it is a necessary adjustment if the government wants to avoid taxing the State Pension.

Understanding Fiscal Drag and Your Paycheck

Fiscal drag is a quiet but powerful force. Let’s say you receive a 5% pay rise this year to help with your energy bills. Because the tax-free personal allowance of £12,570 is frozen, that entire 5% increase is taxed at 20% (for basic rate payers) or 40% (for higher rate payers).

Hello world!

If the allowance were raised to £13,570, it would effectively “shield” that pay rise from the taxman. Without the increase, your “real-term” income—what you actually have left to spend after inflation and tax—often ends up lower than it was the year before. This is why many financial experts refer to the frozen allowance as a “hidden tax” that hits low and middle-income earners the hardest.

How HMRC Tracks Your Earnings Automatically

It is important to remember that HMRC doesn’t need you to tell them when you’ve crossed a threshold. Through the Real Time Information (RTI) system, employers send pay data to HMRC every time you get paid. For pensioners, the DWP shares information directly with the tax office.

If the threshold remains at £12,570 and your income exceeds it, HMRC will simply adjust your Tax Code. You might notice your code change from 1257L to something else. This allows them to collect the tax owed directly from your pension or salary before it even reaches your bank account. This automated system is incredibly efficient, meaning very few people “escape” the tax net created by the frozen thresholds.

The Arguments Against Raising the Limit

If raising the allowance to £13,570 is so popular, why hasn’t the government done it? The answer is purely financial. Each £100 increase in the Personal Allowance costs the Treasury billions of pounds in lost revenue.

The government argues that the money generated from the “stealth tax” of fiscal drag is essential for funding the NHS, social care, and education. Moving the threshold to £13,570 would create a massive hole in the public finances that would have to be filled by either cutting services or raising other taxes, such as VAT or National Insurance. In the current economic climate, the Treasury appears to prefer the “quiet” revenue generated by frozen thresholds over the political fallout of a direct tax hike.

Potential Changes in the Autumn Statement

While there is no official rule change yet for the £13,570 limit, the financial world is looking toward the upcoming Autumn Statement. In the UK, major tax changes are rarely announced mid-year. If a plan to raise the allowance exists, it would likely be unveiled by the Chancellor during a major fiscal event.

Political analysts suggest that as we approach the next general election, a rise in the Personal Allowance could be used as a “sweetener” for voters. Increasing the limit to £13,570 would be a high-impact way to signal that the government is on the side of working families and retirees. Until that red box is opened, however, any specific figures remain speculative.

How to Protect Your Income Without a Raise

Since we cannot rely on the government to raise the tax-free limit to £13,570, it is up to individuals to use the existing rules to their advantage. There are several legal ways to effectively “increase” your tax-free income:

-

Pension Contributions: For workers, paying more into a workplace or private pension reduces your “taxable income.” If you earn £13,570 but put £1,000 into a pension, your taxable income drops back to £12,570, keeping you out of the tax net.

-

Marriage Allowance: If you are married or in a civil partnership and one partner earns less than £12,570, they can transfer £1,260 of their unused allowance to their partner. This can save a couple up to £252 a year.

-

ISAs and Premium Bonds: Ensure your savings are in tax-free wrappers. Interest earned in an ISA doesn’t count toward your Personal Allowance, protecting you from HMRC’s “Simple Assessment” letters.

The Role of the Blind Person’s Allowance

For some, the Personal Allowance is already higher than £12,570. If you are registered as blind or severely sight-impaired, you can claim the Blind Person’s Allowance. This adds a significant chunk to your tax-free limit. For the 2026/27 year, this is set to rise in line with inflation, unlike the standard allowance.

If you qualify, your personal tax-free limit would actually exceed the rumored £13,570 figure. Many people forget to claim this, or are unaware that they can transfer this allowance to a spouse if they don’t have enough income to use it themselves.

What a £13,570 Limit Would Mean for the Economy

Economists are divided on the impact of a threshold rise. Proponents argue that putting more money back into the pockets of consumers would boost spending on the high street, stimulating the economy. They argue that the current freeze is stifling growth because people have less “disposable” income to circulate.

On the other hand, some worry that a sudden jump to £13,570 could be inflationary. If millions of people suddenly have more cash to spend, it could drive up the demand for goods and services, potentially causing prices to rise further. It’s a delicate balancing act that the Treasury has to perform every year.

Preparing Your Finances for 2027

Whether the limit stays at £12,570 or makes the jump to £13,570, the best strategy is preparation. Don’t wait for a letter from HMRC to find out you owe money. Use online calculators to estimate your total income from all sources—pensions, work, and savings interest.

If you find that you are going to be just over the limit, consider if there are any “allowable expenses” you can claim, especially if you are self-employed or a “micro-entrepreneur” using the £1,000 trading allowance. Knowledge is your best defense against unexpected tax bills.

Keeping a Close Eye on Official HMRC Channels

In an era of viral news, it is easy to get swept up in headlines about “New Rules” and “Official Announcements.” However, the only source of truth for your taxes is the official GOV.UK website and the formal announcements made in Parliament.

While the movement for a £13,570 allowance is growing and makes logical sense given the current inflation rates, it remains a “proposal” rather than a “plan” until the Chancellor signs it into law. For now, the £12,570 freeze remains the law of the land, and every UK taxpayer should plan their budget accordingly.