Banking in the United Kingdom is currently experiencing one of its most significant shifts in recent years. As of today, several of the nation’s major financial institutions have officially implemented new cash withdrawal limits specifically tailored for customers over the age of 60. While the digital age has moved many of us toward contactless payments and online banking, a substantial portion of the senior population still relies on physical cash for their day-to-day living. These new regulations are not just a minor update; they represent a fundamental change in how seniors interact with their own money, aimed primarily at tackling the rising tide of sophisticated financial scams.

The confirmation of these changes comes after months of deliberation between the Financial Conduct Authority and the banking sector. The primary goal is protection, yet the implementation has sparked a wide-ranging debate across the country. For many, the ability to walk into a local branch or visit an ATM and withdraw their desired amount of cash is a symbol of financial independence. The introduction of specific caps for the over-60s demographic is a complex balancing act between keeping life-savings safe and maintaining the freedom of access that UK citizens have enjoyed for decades.

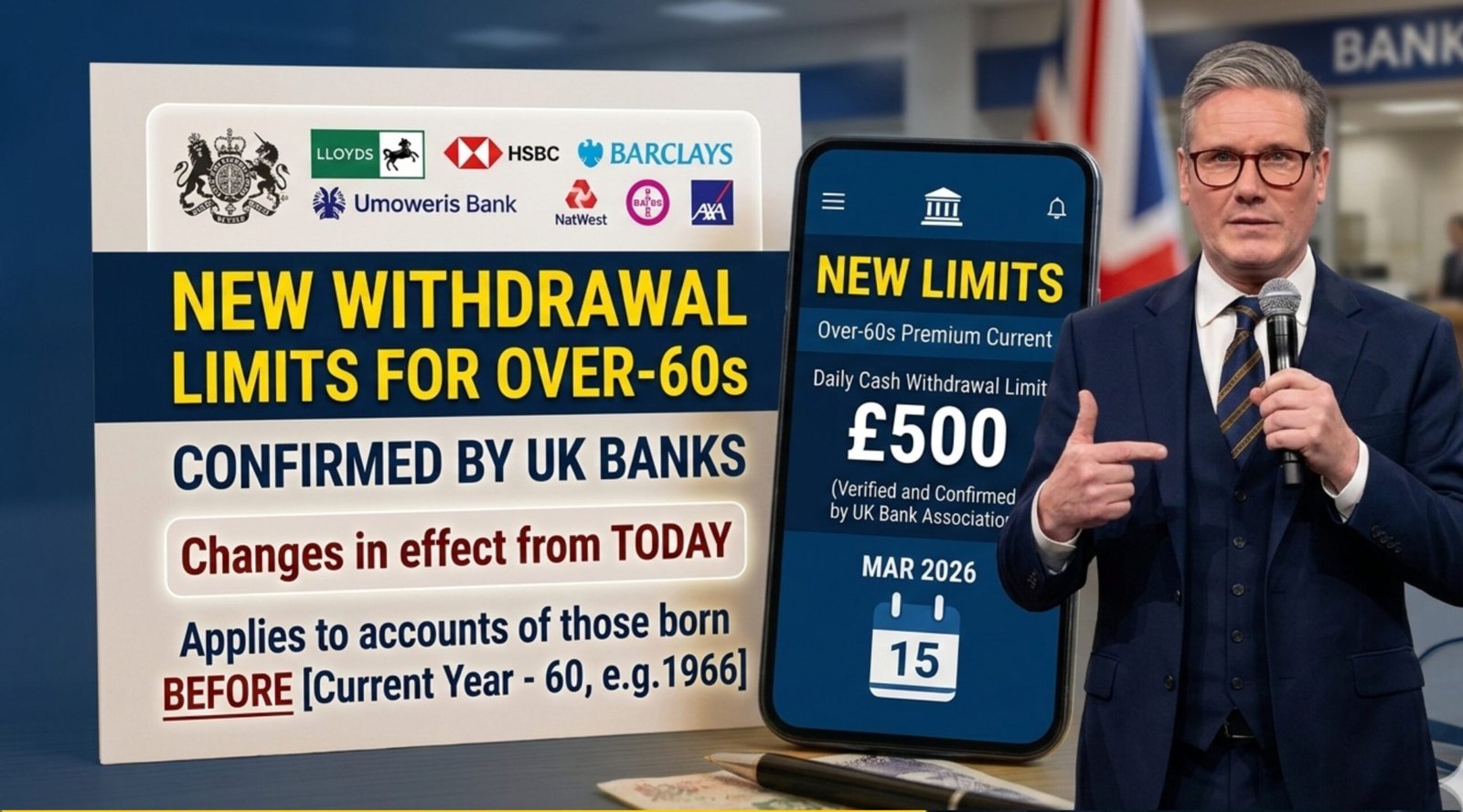

Understanding the Daily Cash Caps

The headline change that most will notice immediately is the new daily limit on ATM withdrawals. For most over-60s accounts, banks have now set a standard daily ceiling of £500. This is a noticeable reduction for those who were previously accustomed to higher limits or who prefer to withdraw larger sums at the start of the week to manage their household budget. The logic behind this specific figure is rooted in fraud prevention. Data shows that “distress withdrawals”—where a victim is pressured by a scammer to hand over cash—often involve sums just above this new threshold.

By capping the daily limit at £500, banks are effectively creating a “cooling-off period.” If a customer is being targeted by a fraudster, the limit prevents the total loss of a large sum in a single transaction. While this might seem like an inconvenience for a genuine customer planning a significant purchase, the banking sector argues that this small barrier is the most effective way to catch fraudulent activity before it becomes catastrophic. It is a digital-age safety net designed for a generation that scammers frequently target.

New Rules for In-Branch Transactions

It isn’t just the ATMs that are seeing changes today. If you plan to visit a high street branch to withdraw a larger sum of money, the process has become significantly more rigorous. For any withdrawal exceeding £2,000, customers over 60 will now be required to provide advance notice—typically 24 to 48 hours. Furthermore, bank staff have been given updated mandates to conduct “well-being checks.” This involves asking more detailed questions about the purpose of the withdrawal to ensure the customer isn’t being coerced.

This particular change has been met with mixed feelings. On one hand, it provides an extra layer of defense against “rogue trader” scams, where seniors are pressured into paying for unnecessary home repairs in cash. On the other hand, many feel that having to justify their spending to a bank teller is an overreach. However, the banks are standing firm, noting that these conversations have already saved millions of pounds in potential losses over the trial periods conducted late last year. The “proof of purpose” requirement is now a standard part of the UK banking experience for senior citizens.

The Rise of the Silver Scams

To understand why these limits are starting today, one has to look at the statistics regarding financial crime in the UK. Seniors are often the primary targets for “courier fraud” and “romance scams,” where the end goal is always to get the victim to withdraw physical cash. Unlike a digital transfer, which can sometimes be “clawed back” by the bank if caught early, once cash leaves a branch or an ATM, it is virtually untraceable. This makes cash the preferred currency of the modern criminal.

The March 2026 changes are a direct response to a 15% rise in cash-based fraud reported in the previous fiscal year. Scammers have become incredibly adept at mimicking official voices, often pretending to be from the police or the bank itself. By slowing down the physical withdrawal process, the DWP and the banking sector hope to give families and bank security teams more time to intervene. It is a structural response to a social problem that has been draining the retirement pots of thousands of UK residents.

Impact on Rural Communities and Access

One of the major concerns raised by advocacy groups is how these limits will affect those living in rural areas. In many parts of Scotland, Wales, and Northern England, bank branches have been closing at an alarming rate. For a senior living in a village with no local branch, a trip to the nearest town is a planned event. If they arrive only to find they cannot withdraw the amount they need for the month due to the new £500 limit, it creates a genuine logistical hardship.

The government has attempted to mitigate this through the “Access to Cash” legislation, which mandates that banks must ensure reasonable access to withdrawal facilities. However, the new limits add a layer of complexity to this. Some banks are suggesting that customers use “Banking Hubs” or the Post Office to bypass some of the stricter ATM caps, but even these facilities will be bound by the new over-60s verification protocols. The shift today highlights the growing “digital divide” and the need for a more nuanced approach to rural banking.

How to Request a Limit Adjustment

Crucially, these new limits are not necessarily set in stone for every single customer. Banks have confirmed that there is a process for individuals to request a “limit uplift” based on their specific circumstances. If you have a legitimate, recurring need for higher cash amounts—perhaps for a specific hobby, a family tradition, or managing a small community group—you can apply to have your daily or weekly limit increased. This usually requires a face-to-face meeting with a personal banker to establish a “trusted profile.”

This flexibility is essential for maintaining the dignity of the senior population. It allows those who are tech-savvy and fully aware of scam risks to maintain their previous levels of freedom. However, the default setting for all accounts has switched to the lower limit as of this morning. If you haven’t proactively contacted your bank to discuss an adjustment, you should assume that the new £500 daily and £2,000 weekly caps are now active on your account.

The Role of Technology in Protection

While the focus today is on physical cash, these changes are part of a broader “Smart Banking” initiative. Many banks are now encouraging over-60s to use mobile apps that feature “Dual Authorization.” This allows a trusted family member or a legal power of attorney to receive a notification on their phone whenever a large withdrawal is attempted. It doesn’t give the family member control over the money, but it acts as a secondary alert system.

This “Second Pair of Eyes” approach is being hailed as the future of senior banking. It combines the independence of the account holder with the security of a modern monitoring system. As these digital tools become more user-friendly, the reliance on restrictive cash limits may eventually decrease. For now, however, the physical caps are seen as the most reliable “hard” barrier against the immediate threat of theft and fraud.

Preparing for the Transition Today

If you are over 60, the best way to handle these changes is to take a proactive look at your upcoming expenses. If you have a major purchase planned for later this month that requires a cash payment, you should contact your bank now to avoid being blocked at the counter. It is also a good time to review your standing orders and direct debits; the more of your regular bills you can move to digital payments, the less you will be affected by the ATM caps.

It is also worth sitting down with your bank’s latest “Terms and Conditions” booklet, which should have arrived in the post or via email recently. These documents detail the specific nuances of how your particular bank is implementing the rules. Some building societies, for instance, may have slightly different thresholds than the major “Big Four” banks. Understanding the specifics of your own provider will prevent any unpleasant surprises during your next trip to the high street.

Financial Independence in the Modern Age

The dialogue surrounding these changes often touches on the concept of “financial elderhood.” In the UK, we are living longer, and our “third act” is more active than ever before. Maintaining financial independence is a key part of aging with dignity. These bank limits, while frustrating to some, are intended to preserve that independence by ensuring that a lifetime of hard work isn’t wiped out by a five-minute phone call from a scammer.

As we move forward into 2026, the definition of “safe banking” will continue to evolve. The changes starting today are a snapshot of a society trying to protect its most experienced members from the dark side of technological progress. By staying informed and adapting to these new protocols, UK seniors can continue to manage their wealth with the confidence that the system is working to watch their back, even if it means an extra check at the teller window.

Looking Toward Future Regulations

Today’s update is likely not the final word on senior banking. As the UK moves closer to a “cash-light” economy, the FCA is constantly reviewing how the transition affects different age groups. There are ongoing discussions about “pensioner-specific” bank accounts that might offer higher interest rates in exchange for accepting certain security restrictions. The goal is to create a bespoke banking experience that acknowledges the unique risks and requirements of the over-60s demographic.

For now, the focus remains on the implementation of these withdrawal limits. The success of this policy will be measured not by how many people are inconvenienced, but by how many millions of pounds are kept safe from criminals. It is a new chapter in British banking, and one that requires both the banks and the public to work together to ensure that “safety” doesn’t come at the cost of “service.”