From this morning, millions of banking customers across the United Kingdom will notice a significant shift in how they access their physical cash. Major high-street lenders, including Lloyds, Barclays, NatWest, and HSBC, have officially implemented new daily withdrawal limits specifically tailored for account holders aged 60 and over. While the move is being framed as a robust defense mechanism against the rising tide of sophisticated financial scams, it marks one of the most substantial changes to personal banking autonomy in recent years.

The introduction of these limits comes after a series of high-level consultations between the Financial Conduct Authority (FCA) and the UK’s leading financial institutions. As of today, the standard daily “unverified” cash withdrawal limit for many over-60s has been adjusted, meaning those wishing to take out larger sums will encounter new protocols, identity checks, and “well-being” conversations at the teller’s desk.

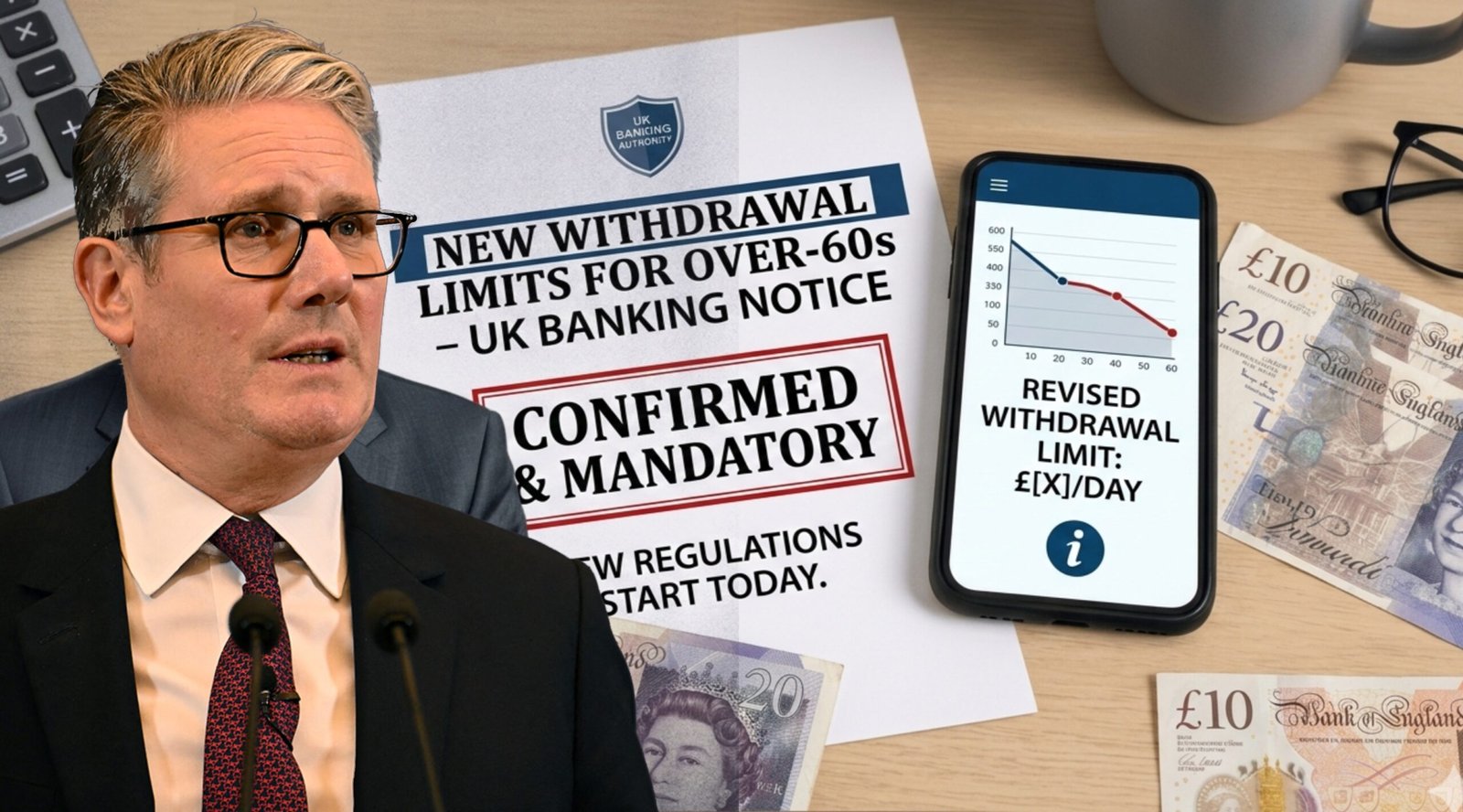

The New Daily Thresholds Explained

For the majority of customers in this age bracket, the most immediate change is the cap on ATM withdrawals. While many accounts previously allowed up to £500 or £800 to be taken from a machine daily, several banks have now lowered this to £300 for customers over 60 unless a specific “high-limit” request has been pre-authorized.

UK Ends the 67 Rule – New State Pension Age Officially Approved

Inside the branch, the changes are even more pronounced. For withdrawals exceeding £1,000, customers will now be required to undergo a brief but mandatory security interview. This isn’t about the bank being nosy regarding your spending habits; rather, it is a standardized procedure to ensure that the customer is not being coerced by a third party or acting under the influence of a fraudulent phone call.

Protecting Seniors from Evolving Scams

The primary catalyst for these changes starting today is the alarming rise in “bank impersonation” and “courier fraud.” Data from Action Fraud suggests that people over 60 are disproportionately targeted by criminals who pretend to be police officers or bank security staff. These scammers often pressure victims into withdrawing their life savings in cash, claiming the money needs to be “inspected” or “moved to a safe account.”

By lowering the immediate withdrawal limit and introducing a human intervention point for larger sums, banks are creating a vital window of time. This “reflective period” allows bank staff to spot the tell-tale signs of distress or coaching. If a customer is on their mobile phone while at the counter or appears unusually anxious, staff now have the explicit authority to pause the transaction for further verification.

Digital Notifications for Family Members

A groundbreaking feature accompanying today’s rollout is the “Trusted Contact” notification system. Customers over 60 now have the option to link their account to a trusted family member or solicitor. If a withdrawal attempt is made that exceeds a certain personal limit or occurs at an unusual time or location, the trusted contact receives an instant alert via a mobile app.

This is an opt-in service, respecting the independence and privacy of the account holder. However, for those who worry about their own vulnerability or those managing the early stages of cognitive decline, this digital safety net offers immense peace of mind. It ensures that even if a scammer manages to convince the account holder, a second pair of eyes is alerted before the funds are gone.

The Role of the Banking Protocol

Today’s changes also see an expansion of the “Banking Protocol,” a rapid-response scheme that links bank branches directly with local police forces. Under the new rules, if a branch manager suspects a customer is in the middle of being defrauded, they can trigger an emergency call that prioritizes a police arrival at the branch.

Previously, this was used only in extreme circumstances. From today, the threshold for triggering this protocol has been lowered for customers over 60. This proactive stance is intended to catch “couriers” who are often waiting nearby to collect the cash from the victim, turning a bank branch from a scene of a crime into a trap for the criminals.

Balancing Independence and Safety

There has been significant debate in the lead-up to today regarding the “nanny state” feel of these regulations. Many over-60s in the UK are financially savvy, tech-literate, and perfectly capable of managing their own money without interference. Banks have been careful to state that these measures are not a “ban” on spending, but a change in the process of accessing cash.

To address concerns about autonomy, banks are offering “White-Listed Transactions.” If you have a regular need for large amounts of cash—perhaps for a hobby, a specific local business, or giving to grandchildren—you can register these “known purposes” with your bank. Once registered, the enhanced questioning is bypassed, allowing you to maintain your lifestyle without repetitive interrogation.

Impact on Rural Communities

For those living in rural parts of the UK where bank branches have vanished, today’s changes will be felt most acutely at the Post Office. Through the “Banking Framework” agreement, Post Office counters will also be enforcing these new withdrawal limits and questioning protocols.

This is a crucial point, as many seniors rely on their local Post Office as their primary point of financial contact. Staff at these locations have undergone intensive training over the last few months to ensure they can handle these sensitive conversations with the same level of care and professional skepticism as a high-street bank manager.

The Decline of the “Cash Under the Mattress”

UK banks are also using today’s launch to encourage a move away from keeping large sums of physical cash at home. Beyond the risk of scams, the rise in “distraction burglaries” remains a concern for the over-60 demographic.

As part of the new limits, banks are offering free “Safe Spending” workshops and helping customers set up secure digital transfers for things like home repairs or car purchases. By making digital payments more accessible and less intimidating, they hope to reduce the physical necessity for large cash withdrawals that put seniors at risk.

How to Prepare for Your Visit Today

If you are planning to visit your bank today or later this week to withdraw a significant sum, it is advisable to bring a form of photo ID, even if you are a regular at the branch. With the new protocols in place, “knowing the face” is no longer enough for high-value transactions; the digital audit trail requires formal verification.

If the money is for a specific purpose, such as paying a tradesperson, having an invoice or a written quote on hand will satisfy the new “verification of intent” requirements almost instantly. The more transparency you provide, the faster the transaction will be processed.

Medical Exemptions and Power of Attorney

For customers who may find the new questioning process stressful due to health reasons, there are provisions in place. Those with a registered Power of Attorney (LPA) will find that their attorneys can pre-authorize withdrawals, making the process smoother for the account holder.

Additionally, banks have introduced “Quiet Hours” and private booths for these discussions. If a customer feels overwhelmed by the busy environment of a branch, they can request to speak to a “Senior Account Guardian” in a private setting to complete their withdrawal away from the eyes and ears of other customers.

The Future of Age-Related Banking

Today is just the beginning of a broader trend toward “dynamic banking” in the UK. Industry experts predict that within the next few years, withdrawal limits won’t just be based on age, but on individual “spending DNA” powered by AI. This would mean the bank knows what is “normal” for you and only intervenes when something truly outliers occurs.

For now, the focus remains on the over-60s as a high-priority group. The government has signaled that if these measures are successful in reducing fraud losses over the next twelve months, they may be adjusted or even expanded to other age groups who are showing signs of vulnerability to specific types of cybercrime.

A Community-Led Approach to Finance

The success of today’s changes will ultimately depend on the relationship between the banks and their customers. It requires a level of trust that the bank is acting as a protector, not a gatekeeper. Community groups and charities like Age UK have been involved in the design of these protocols to ensure they are handled with empathy.

The message from the UK’s financial sector today is clear: cash is still yours to use, but the banks are going to take an active role in making sure it stays in your pocket and out of the hands of criminals. It may take some time to get used to the extra questions at the counter, but in an era where scammers are increasingly ruthless, a little bit of extra “banking friction” might be the best defense we have.

Staying Informed and Secure

As these rules take effect starting today, it is important to stay informed through your bank’s official channels. Be wary of any emails or texts claiming to be about “your new withdrawal limits” that ask for your PIN or password—ironically, scammers are already trying to use the news of these very safeguards to trick people.

Your bank will never ask you for your full security details over the phone or via text to “authorize” your new limits. If you have any doubts about how your account is affected, the best course of action is to walk into your local branch and speak to a member of staff face-to-face.